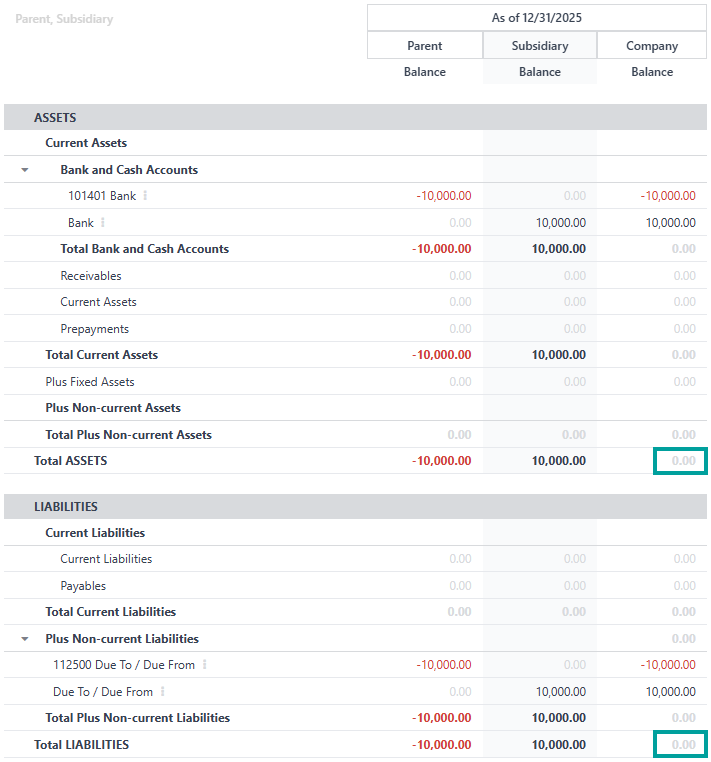

When I run consolidated financial reports, the "owed to" and "owed from" amounts should be eliminated, since they cancel each other out.

Odoo is the world's easiest all-in-one management software.

It includes hundreds of business apps:

- CRM

- e-Commerce

- Contabilidad

- Inventario

- PoS

- Proyecto

- MRP

Se marcó esta pregunta

1

Responder

738

Vistas

Inter company transactions are best handled via the Transfer of funds through a DUE TO / DUE FROM Account.

We recommend this approach because:

- it closely matches the steps in the real world.

- it follows accounting best practices many Book-keepers, Accountants and Controllers will be familiar with.

- no AP or AR is involved.

- no special account types are needed.

- a reconcilable Journal Entry for each Bank Account involved is created to match the bank statement withdrawal / deposit activity.

- you can show the DT/DF account balance(s) anywhere on the Balance sheet.

Some businesses have two accounts. For a given Company A, the first account - DUE TO B - is a liability account that represents the money Company A owes to Company B. The second account - DUE FROM B - is an asset account that represents the money Company B owes to Company A.

Some businesses have one account. Company A would create a liability account DUE TO / DUE FROM B to represent both things. A positive balance means Company B owes Company A money. A negative balance means Company B owes Company A money.

My example will use a single account.

1. Setup the Accounts in each Company. Here, we have two companies - PARENT and SUBSIDIARY.

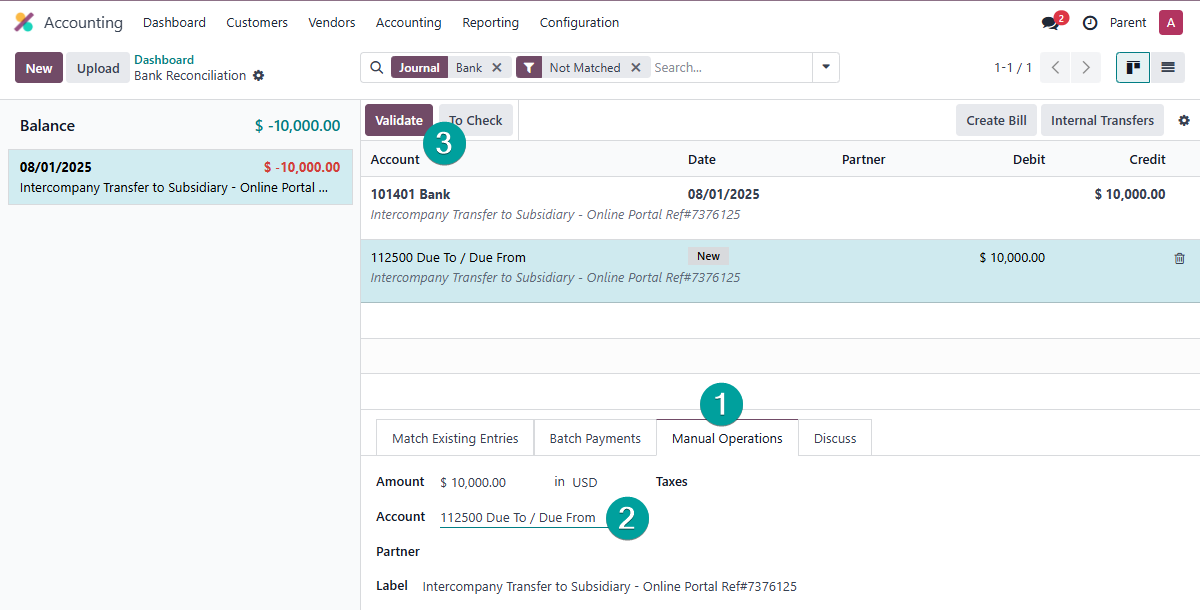

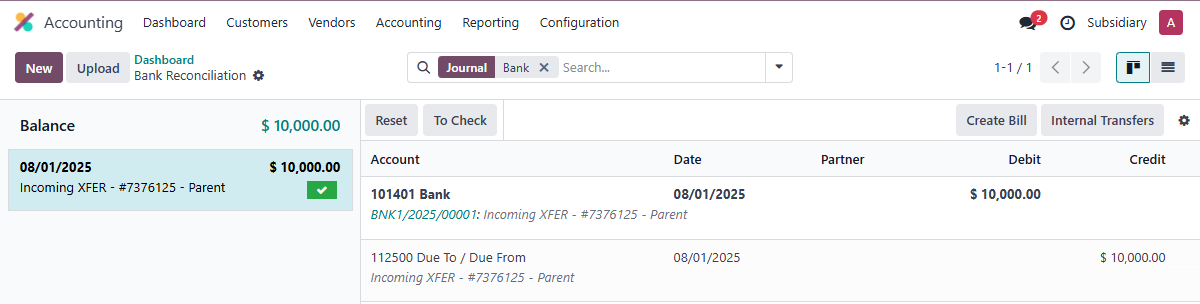

2. When reconciling your bank statement, you will need to select this account as the counterpart for both the withdrawal from the Parent and the deposit to the Subsidiary

Reconciling the Parent side:

Reconciling the Subsidiary side:

The Consolidated Balance Sheet after funding - note the cash sent / received and liability / asset [negative liability] cancel each other out:

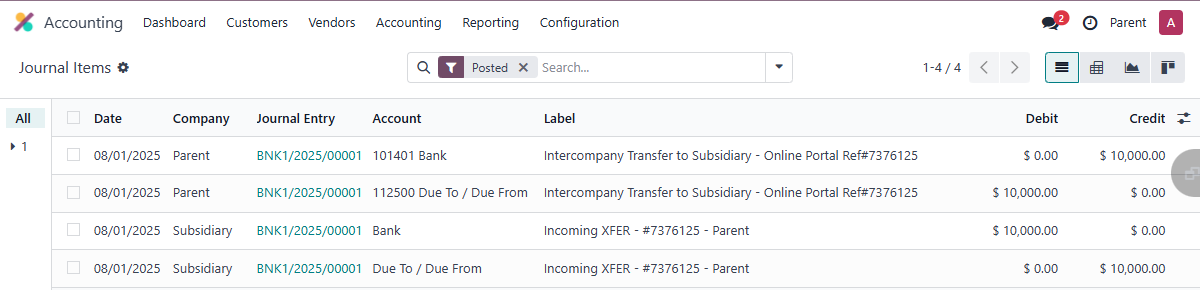

Journal Entries created:

¿Le interesa esta conversación? ¡Participe en ella!

Cree una cuenta para poder utilizar funciones exclusivas e interactuar con la comunidad.

Inscribirse| Publicaciones relacionadas | Respuestas | Vistas | Actividad | |

|---|---|---|---|---|

|

3

ene 25

|

24922 | ||

|

|

1

jul 25

|

741 | ||

|

3

nov 25

|

685 | ||

|

2

ago 25

|

1114 | ||

|

2

jul 25

|

2872 |