What is an asset?

The assets of a company are defined as the set of goods, rights and other resources that a company owns, in other words, it has economic control over them. These can be office equipment, such as computers, furniture or the office itself, as well as patents (intellectual property) or shares.

There are two types of assets, fixed and current. Current assets are those goods or rights that can be converted into money. Some examples of these would be accounts receivable from customers or the company's merchandise.

Fixed assets are those that have a decreasing value as they are used, i.e., they have a useful life and are depreciated as time goes by. The depreciation of these assets will depend on three factors: use, time and technological obsolescence.

What is depreciation?

In simple terms, depreciation is the reduction in the value of a tangible asset. As mentioned, the depreciation of a tangible asset can be due to 3 different causes: use, time and obsolescence.

Depreciation can be calculated in different ways according to its type, although there are different methods that we can find, all of them are valid. The four general methods of depreciation are: straight line, sum of digits, declining balance or reduction of data, units of production and accelerated depreciation.

Straight-line depreciation consists of dividing the value of the asset equally over its useful life. This method is reflected graphically as a decreasing straight line. The calculation is simple: subtract the residual value from the cost of the equipment and divide this result by the estimated useful life. The residual value is understood as the price for which it could be sold once its estimated useful life is over.

Declining-balance depreciation, unlike straight-line depreciation, varies over time. In this case, the value of the assets decreases by a greater percentage in the first years and their depreciation decreases as time progresses. This depreciation is calculated by multiplying the residual value by the decline factor.

How to calculate depreciation in Odoo?

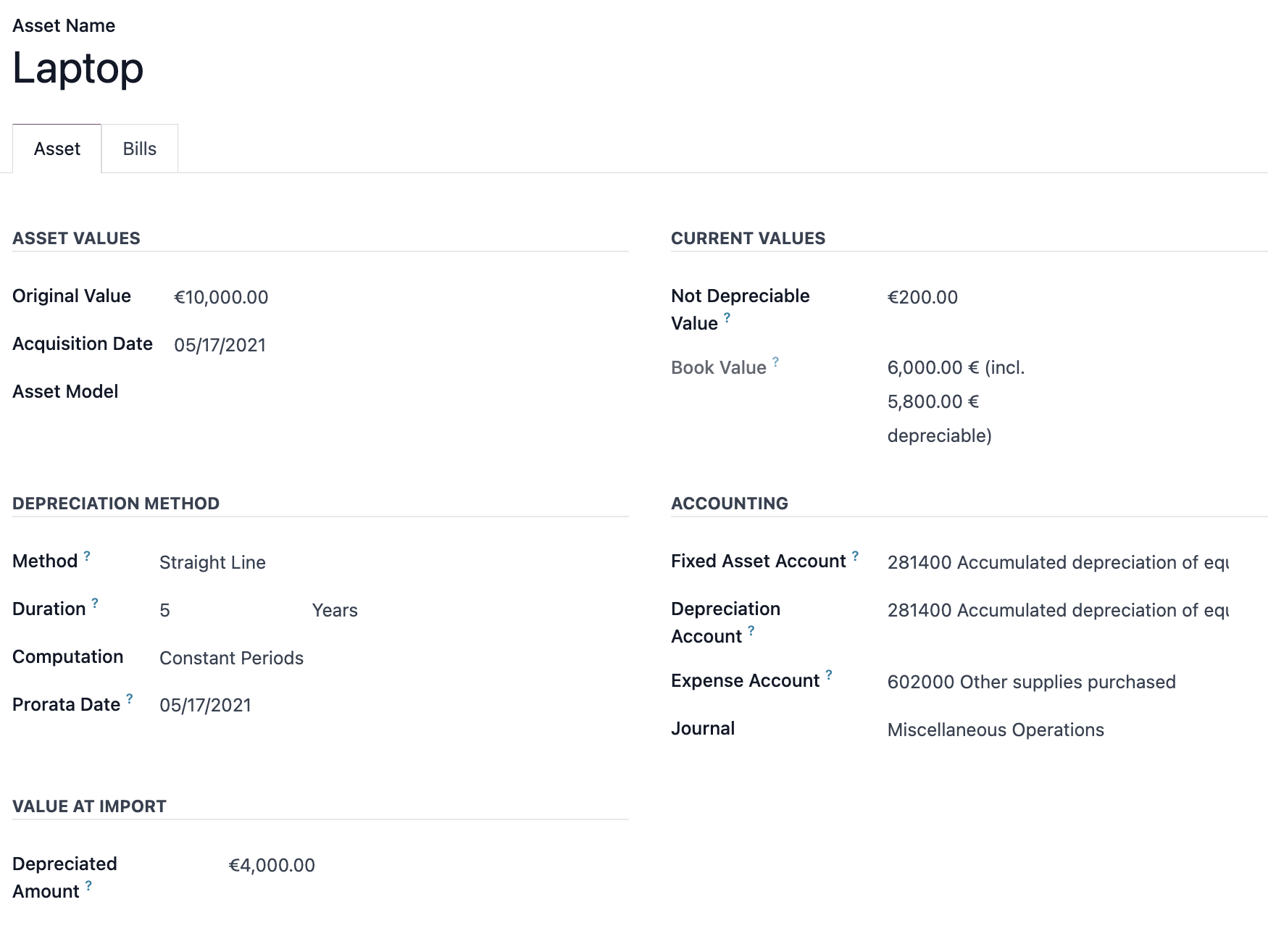

To configure depreciation in an Odoo database, the first thing to do is to have the accounting application installed. In the accounting menu you will find the access to the assets, where we will configure the assets as well as their depreciation method. When creating the depreciation model for each asset we can also create the account on which to depreciate the asset and thus have a global view both in the account and in the general ledger.

We name the asset to depreciate; the method: straight line, declining or declining and straight line. The original value, the date of acquisition of the asset, the non-depreciable value and the amount already depreciated, as well as the accounts in which to depreciate the asset will be the priority fields.

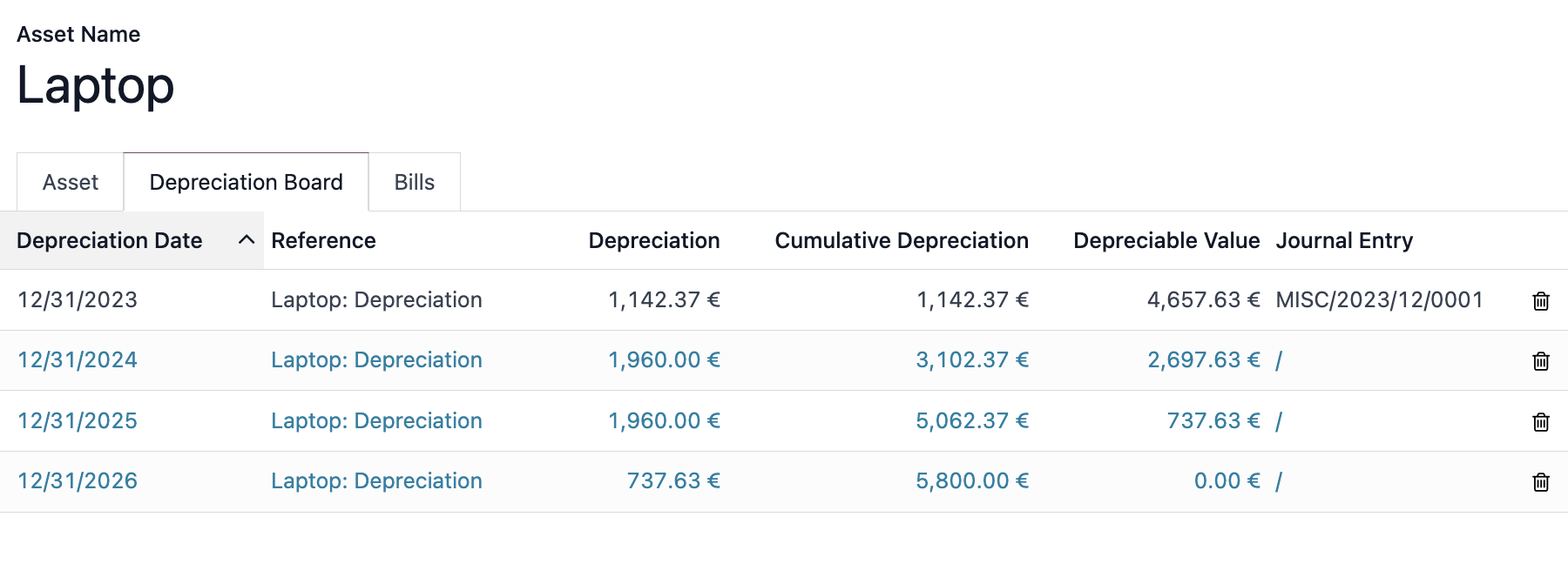

Thanks to these data Odoo will make the calculation and display a table with the depreciation of the asset. In case of coming from a previous system in which the amount already depreciated was registered, this will be directly discounted, thus, the amounts already depreciated in the past will have an entry automatically created and published by the system.

In the same way, these already depreciated assets will be included in the opening entry. By entering the asset lines with the amounts already depreciated, the system will directly match the asset balances with the amounts already depreciated in the previous management system. In addition, with the depreciation calculation, upcoming depreciations will be posted automatically.

Purchases of new assets will be linked to the assets. That is, we will be able to link the purchase invoice of any asset, for example, office supplies, to the asset, so that we can navigate between invoices and assets to see the depreciation of the assets.

Finally, within the functions included in the system, we find the asset models and the analytical distribution. It is possible to create templates for when new assets of the same type that we already have registered enter, for example, a new computer. With the models, simply adding it in the model will do all the management and calculations, as well as the publication of the accounting entries. All depreciations can be included in the analytical distribution for a more accurate expense control.

Asset management and depreciation