LAST UPDATED: October 2022 (Odoo 16)

Inter company transactions are best handled via the Transfer of funds through a DUE TO / DUE FROM Account.

We recommend this approach because:

it closely matches the steps in the real world.

it follows accounting best practices many Book-keepers, Accountants and Controllers will be familiar with.

a transfer can be printed as a check, in case funds need to be moved this way

no AP or AR is involved.

no special account types are needed.

a reconcilable Journal Entry for each Bank Account involved is created to match the bank statement withdrawal / deposit activity.

bank statements (no lines needed, just starting balances) can be created to compare and record the end of period balance in the DT/DF account(s).

bank statements (lines manually added) can be used to reconcile each DT/DF account.

you can show the DT/DF account balance(s) anywhere on the Balance sheet.

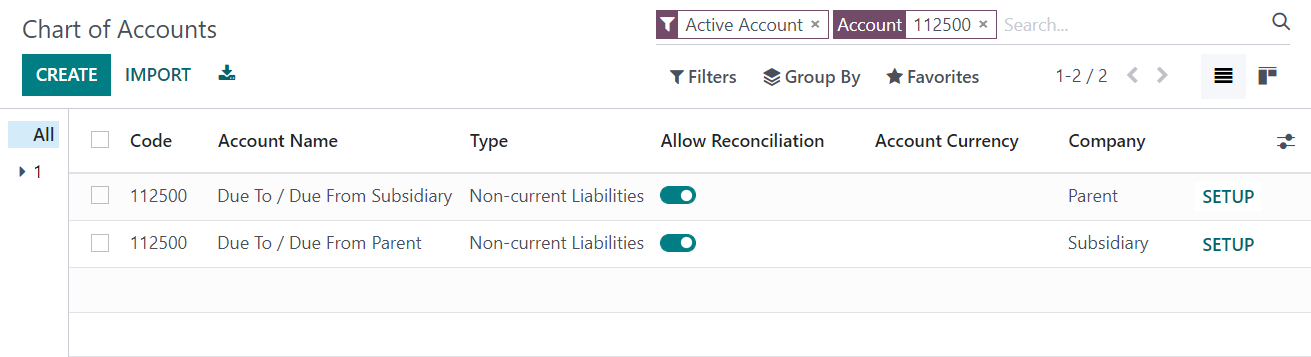

Some businesses have two accounts. For a given Company A, the first account - DUE TO B - is a liability account that represents the money Company A owes to Company B. The second account - DUE FROM B - is an asset account that represents the money Company B owes to Company A.

Some businesses have one account. Company A would create a liability account DUE TO / DUE FROM B to represent both things. A positive balance means Company B owes Company A money. A negative balance means Company B owes Company A money.

My example will use a single account.

1. Setup the Accounts in each Company. Here, we have two companies - PARENT and SUBSIDIARY.

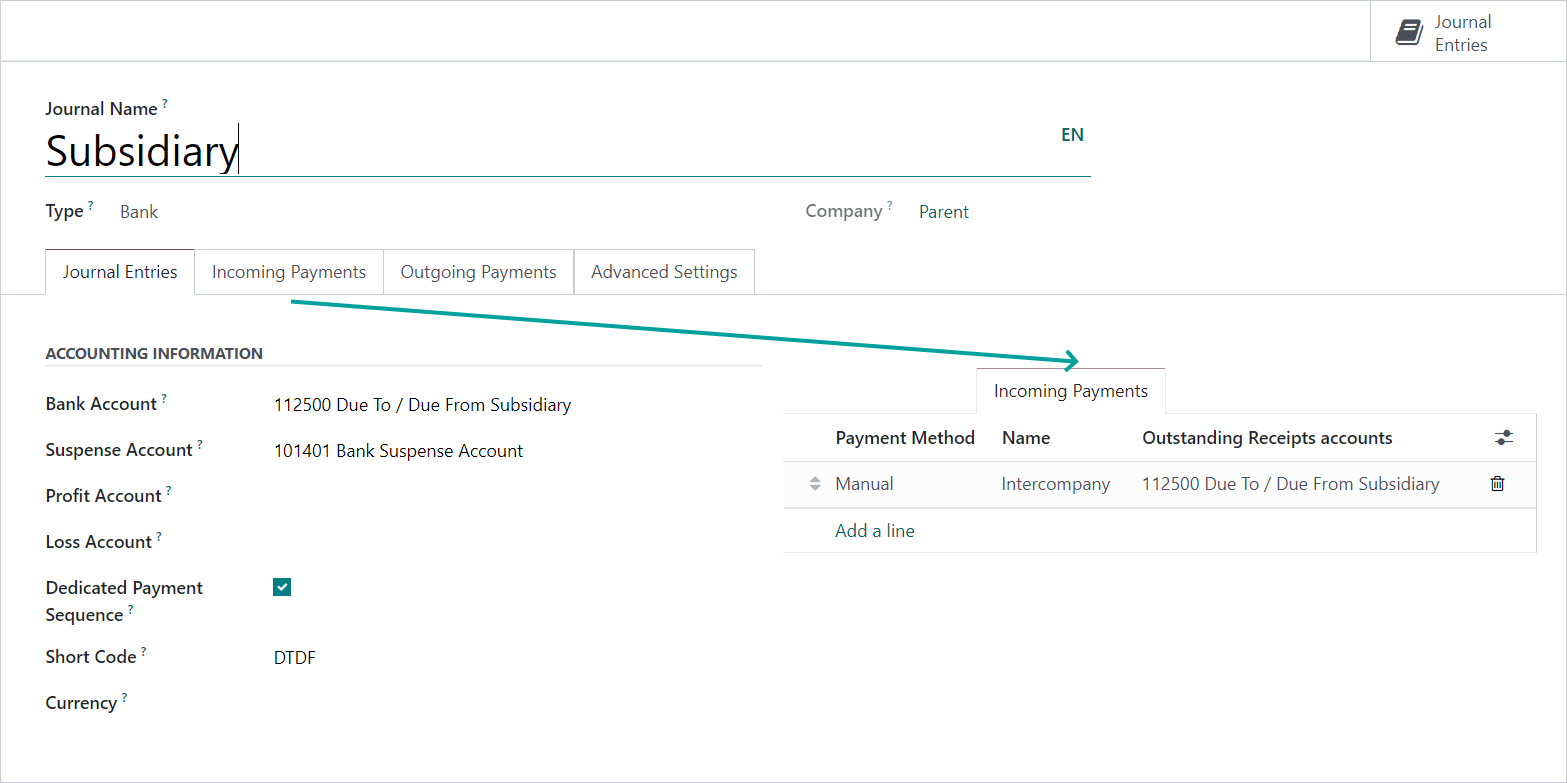

2. Setup a Journal in each Company.

The Journal in Parent is named "Subsidiary" to indicate the flow of funds to and from the subsidiary:

The Journal in Subsidiary is named "Parent" to indicate the flow of funds to and from the Parent:

(set the Bank and Outstanding Accounts to 112500 similar to the prior Journal)

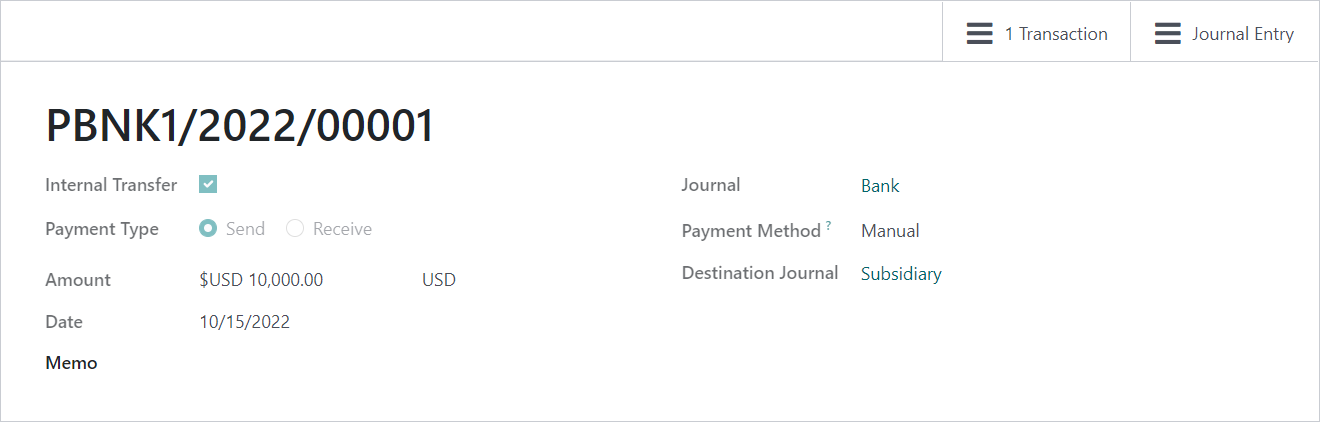

3. For each funding transaction, transfer funds in both Companies:

In the Parent, fund the Subsidiary (transfer from the Bank to the Subsidiary):

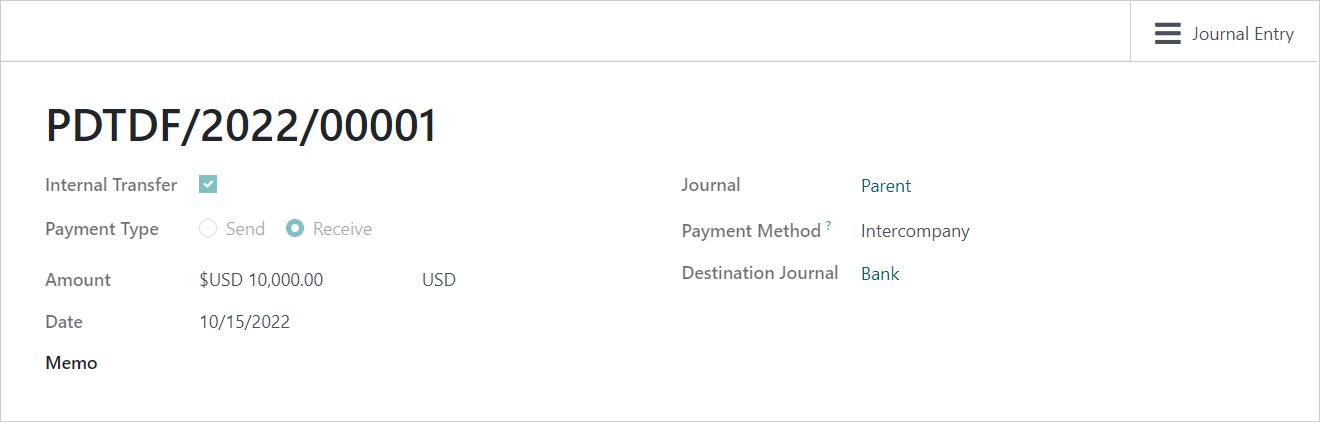

In the Subsidiary, receive the funds from the Parent (transfer from the Parent to the Bank):

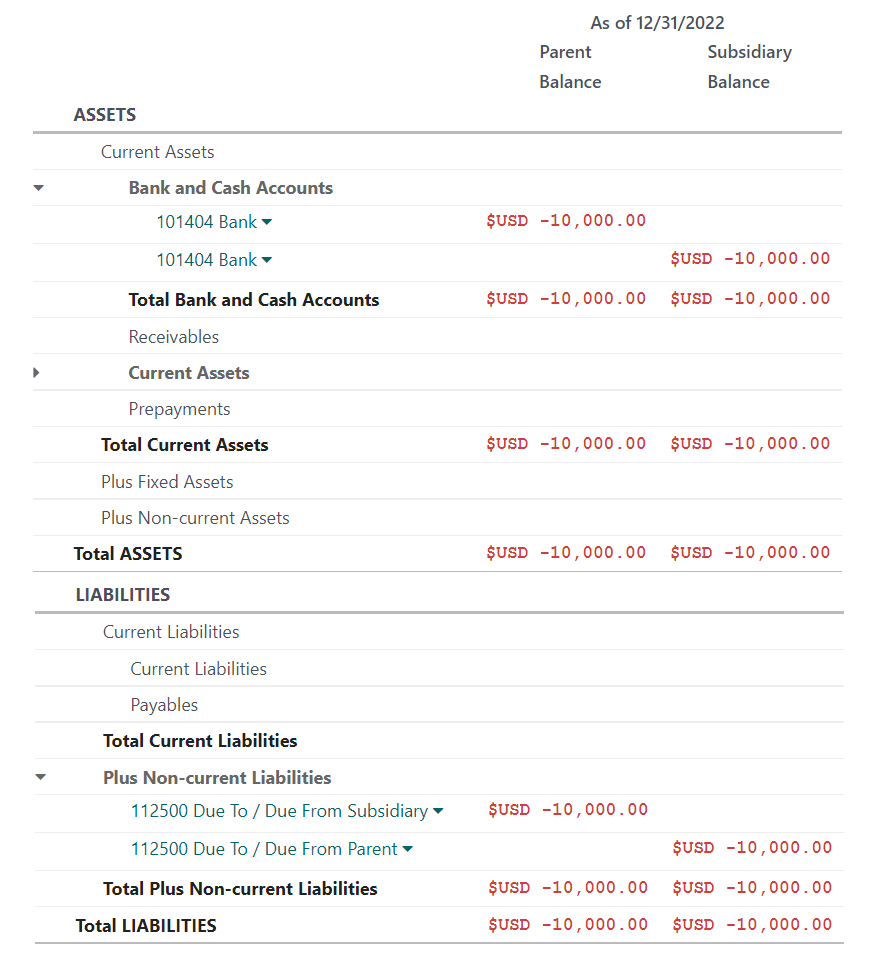

The Consolidated Balance Sheet after funding - note the cash sent / received and liability / asset [negative liability] cancel each other out:

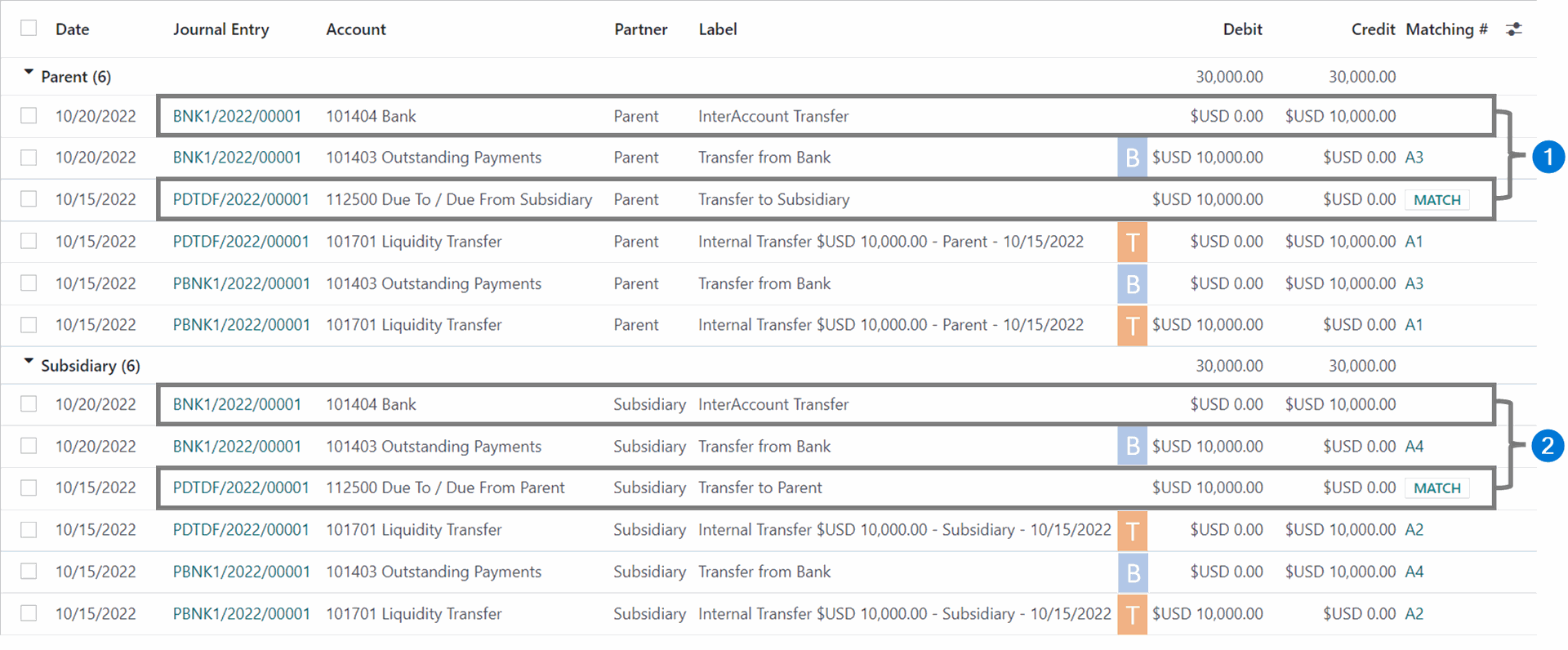

Journal Entries that were created:

1 = in the Parent Company, fund the Subsidiary from Bank

2 = in the Subsidiary Company, fund the Bank from the DT/DF Account

B = cleared and matched during Bank Reconcilation

T = cleared and matched during Internal Transfer Creation

Hi, I have a similar question, whats the practice for treating an expense paid by parent company on behalf of the subsidiary company?

I'm currently recording this is as:

Parent

Dr. Loan to Subsidiary

Cr. Bank

Subsidiary:

Dr. Payable/Expense

Cr. Loan from Parent

the subsidiary is in a different country so its accounts are filled independently there. Because the above does not create any directly traceable funds transfer between the entities is this method valid?